Introduction

Egypt’s Income Tax Law and Executive Regulations impose withholding tax (WHT) on a wide range of cross-border payments. However, one of the most complex and frequently misunderstood areas relates to the classification and taxation of:

Software payments

Royalty and licensing fees

Technical and consultancy services

Misclassifying these payments can lead to over-withholding, disputes with the Egyptian Tax Authority (ETA), rejected treaty-benefit claims, and exposure to retrospective adjustments.

This guide clarifies how Egyptian tax law treats each type of payment and how companies can avoid costly misunderstandings.

1. WHT Treatment of Software Payments in Egypt

Software is one of the most challenging areas because the tax treatment depends on the rights granted.

Egypt distinguishes between:

1.1 Standard Software / SaaS (No Transfer of Rights)

Examples:

Cloud subscriptions

Online platforms

Usage-based software

ERP/CRM access

WHT Treatment:

If the software is used without granting rights to reproduce, modify, or distribute, then:

✔ It is treated as a service, not a royalty

✔ WHT may apply only if the service is performed inside Egypt

✔ Offshore-only access may qualify for 0% WHT

Risk:

If the contract is vague, ETA may reclassify it as a royalty and impose 20% WHT.

1.2 Software License with Usage Rights (Limited License)

If the license allows use only, but no reproduction or distribution:

WHT Treatment:

Could be treated as a royalty

Typically 20% WHT under domestic law

Treaty rates may reduce to 0–10%

Key factor:

Whether the agreement grants limited intellectual property (IP) rights.

1.3 Software with Rights to Copy, Modify, or Distribute

Examples:

OEM agreements

White-label software

Reseller rights

Development licenses

WHT Treatment:

✔ Always treated as a royalty

✔ Subject to 20% WHT under Egyptian law

✔ Treaty may reduce rate but Beneficial Ownership and TRC required

2. WHT Treatment of Royalty Payments

Egypt defines royalties broadly to include payments related to:

Intellectual property (IP)

Patents, trademarks, copyrights

Software rights

Know-how

Technical IP licensing

WHT Rate:

20% domestic rate (Article 56)

Treaty rate may reduce to 10%, 5%, or even 0%

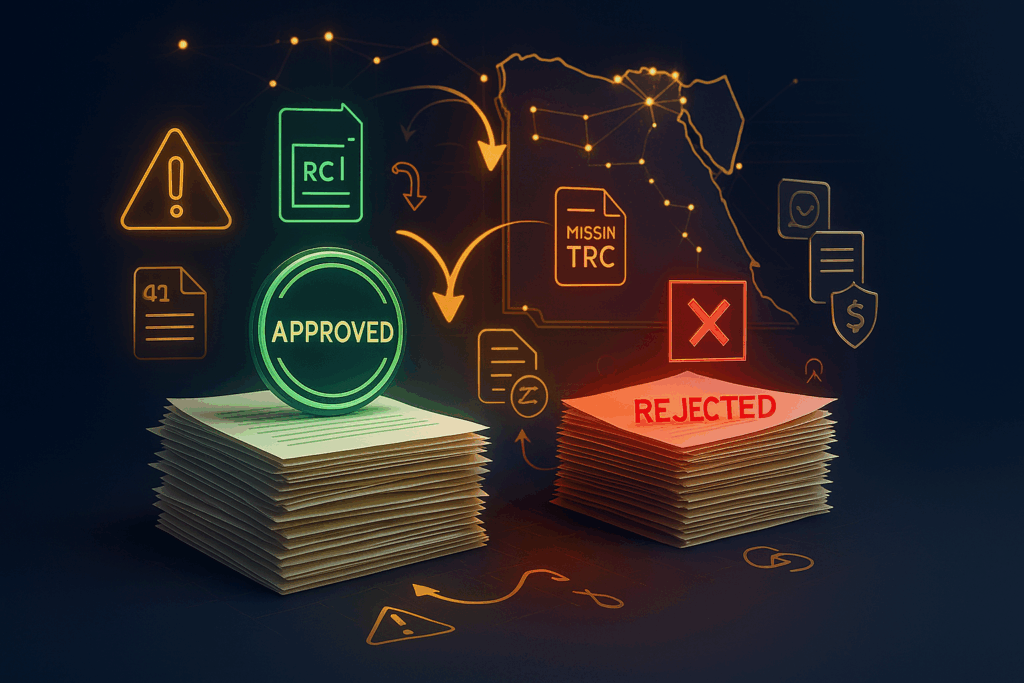

To apply treaty benefits, the foreign recipient must provide:

✔ Valid Tax Residency Certificate (TRC)

✔ Proof of Beneficial Ownership

✔ No Permanent Establishment (PE) in Egypt

ETA Focus Area:

Royalties are heavily scrutinized — especially agreements involving software and technology companies.

3. WHT Treatment of Technical Services

Technical services include:

Consulting

Engineering

IT services

Management support

Training

Installation/implementation

Outsourced operations

Key determinant:

Where are the services performed?

3.1 Services Performed Inside Egypt

WHT Treatment:

✔ Subject to WHT (20% domestic rate unless treaty applies)

✔ Regardless of where the provider is based

3.2 Services Performed Outside Egypt (Fully Offshore)

Examples:

Remote support

Online consulting

Cloud-based development

Non-resident experts advising from abroad

WHT Treatment:

✔ Often 0% WHT

✔ Must be proven with documentation (emails, logs, deliverables, timesheets)

ETA requires clear evidence that no work was performed in Egypt.

3.3 Mixed Services (Onshore + Offshore)

If part of the work is done inside Egypt:

✔ Onshore portion → WHT applies

✔ Offshore portion → May qualify for exemption

A detailed cost split and evidence is necessary.

4. The Role of Double Tax Treaties

Egypt has over 60 treaties, each with specific definitions of:

Royalties

Technical services

Business profits

Permanent Establishment (PE) thresholds

Treaties can:

✔ Reduce WHT

✔ Change classification

✔ Exempt offshore services

Key requirements:

TRC

Beneficial Ownership

Treaty alignment with contract

Proof of no PE in Egypt

5. Common Misinterpretations and ETA Challenges

❌ “Software is always a service.”

Wrong — depends on rights granted.

❌ “Cloud subscriptions are royalty-free.”

True only if no IP rights are granted.

❌ “All technical services are taxable.”

Not true — offshore-only services may be exempt.

❌ “A treaty automatically gives reduced WHT.”

No — TRC + Beneficial Ownership are required.

❌ “Invoices alone prove offshore service.”

ETA requires strong evidence of offshore performance.

6. Best Practices for Accurate WHT Classification

✔ Define software rights very clearly

✔ Separate service from licensing fees in contracts

✔ Provide evidence of offshore work

✔ Maintain documentation supporting classification

✔ Conduct treaty analysis for every payment

✔ Include a clear WHT clause (gross-up or net-of-tax)

✔ Ensure consistency between:

Contract

Invoice

Payment proof

Form 41

Classification

Conclusion

Software, royalty, and technical service payments are among the most complex areas of Egypt’s withholding tax system. Correct interpretation requires understanding both domestic law and treaty rules, as well as the actual commercial substance behind each transaction.

With clear contracts, proper documentation, and accurate classification, multinationals can avoid disputes with the Egyptian Tax Authority and ensure full WHT compliance.