Introduction

Withholding Tax (WHT) refunds in Egypt are often seen as complex, time-consuming, and uncertain.

Many multinational companies either give up or fail to submit complete, compliant documentation leading to rejections, delays, or reduced refund amounts.

However, a well-structured approach can transform the process from a challenging obligation into a successful recovery of significant cash.

This case study outlines how one multinational company managed to secure a full WHT refund in Egypt by applying best practices across documentation, treaty interpretation, and engagement with the Egyptian Tax Authority (ETA).

1. Background of the Multinational Group

The company in this case is a global technology and engineering group operating across more than 20 countries, including Egypt.

The Egyptian subsidiary regularly made payments to its parent and affiliate companies for:

Technical support

Cloud-based services

Software licensing

Regional management assistance

WHT was applied at the default domestic rate of 20%, even though several payments qualified for reduced treaty rates or full exemption.

Over three years, the group accumulated a substantial refundable balance.

2. The Challenge: Why the Refund Was Initially at Risk

The company faced multiple obstacles that commonly lead to refund rejection:

❌ Missing Beneficial Ownership (BO) documentation

❌ No clear evidence that services were performed offshore

❌ Contract wording that mixed royalties with pure services

❌ Inconsistent classification between invoices and agreements

❌ TRC issued after payment dates

❌ No detailed supporting deliverables

These weaknesses were enough for ETA to deny or significantly reduce the refund.

3. The Approach: Building a Strong and Compliant Refund File

The company engaged a specialized tax advisory team to restructure the entire refund case using a three-pillar strategy:

3.1 Contract & Classification Review

Each agreement was reviewed and rewritten (where possible) to:

Separate service fees from software or IP-related fees

Provide clear descriptions of scope, deliverables, and offshore activities

Remove language that could trigger royalty reclassification

Add explicit WHT-treaty clauses

Include gross-up mechanisms when applicable

This ensured the classification aligned with treaty articles, ETA interpretations, and OECD principles.

3.2 Building Strong Evidence of Offshore Service Performance

To justify 0% or reduced WHT exposure, the company compiled:

Work logs

Emails and project trails

Meeting notes

Ticketing system exports

Cloud-service activity reports

Technical documentation

Screenshots of remote session logs

Timesheets for each offshore expert

This demonstrated that work was executed outside Egypt.

3.3 Treaty Analysis and Documentation

For each transaction type, the advisory team prepared:

Beneficial Ownership analysis

Treaty Article mapping (Article 7, 12, or 14 depending on service type)

Explanation of why the foreign entity does not have a Permanent Establishment in Egypt

A full treaty-benefit memo for ETA

In addition, the foreign recipient submitted:

✔ Valid Tax Residency Certificate (TRC) for each fiscal year

✔ Subsidiary-level financial statements

✔ Proof of substance (employees, office, governance)

4. Submission to the Egyptian Tax Authority

The refund file was submitted with:

A master summary

A detailed reconciliation with Form 41 data

Payment proofs

Supporting agreements

All treaty and BO justifications

Organized documentation in chronological order

The key success factor:

The file was structured as if prepared for an audit not just a refund request.

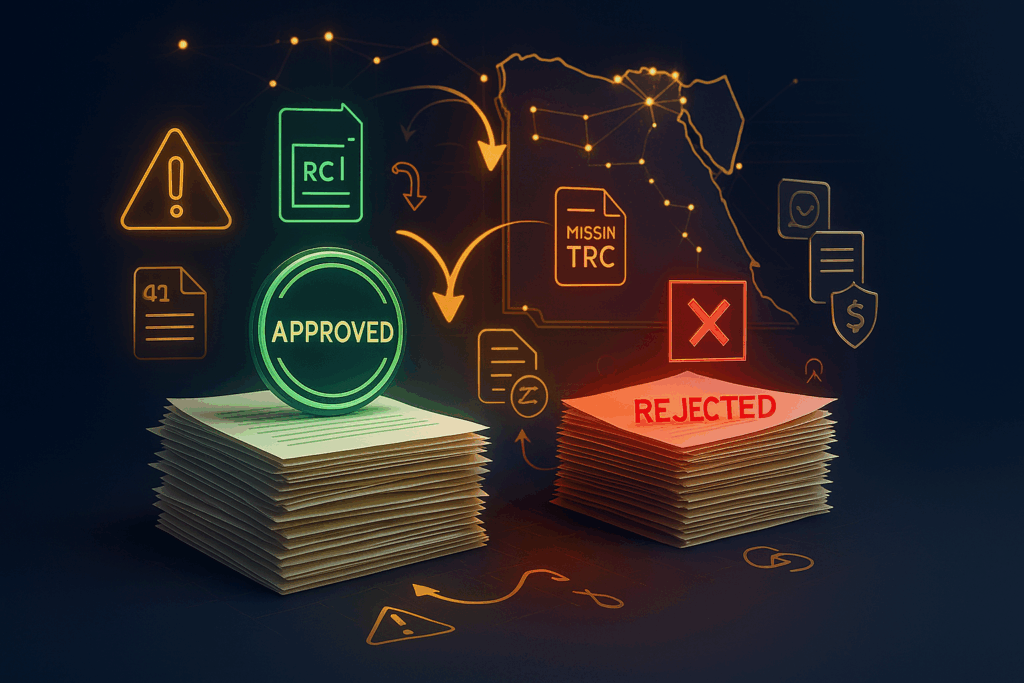

5. The Result: Full Refund Approved

After two rounds of queries and clarifications, the ETA:

✔ Accepted the classification of all service transactions

✔ Rejected a reclassification attempt from “services” to “royalties”

✔ Approved treaty benefits under the applicable DTT

✔ Confirmed no PE existed for the foreign service provider

✔ Issued a full refund for the three-year period

Total amount refunded: 100% of the requested value.

This outcome set a precedent within the group for all future payments and refund claims.

6. Key Lessons from This Case

1. Contracts are the foundation of WHT outcomes

Poorly written agreements are the #1 reason refunds fail.

2. Offshore performance must be proven not assumed

ETA requires hard evidence.

3. Treaty benefits are not automatic

BO + TRC + substance are essential.

4. Classification must match invoices and underlying reality

5. Proactive documentation prevents disputes

Conclusion

This case demonstrates that successful WHT refunds in Egypt are not only possible they are achievable when approached with discipline, technical accuracy, and complete documentation.

A structured file, backed by treaty logic and strong BO evidence, significantly increases the likelihood of approval and reduces the dispute cycle with the ETA.

If replicated well, this strategy allows multinationals to recover millions in wrongly withheld taxes and maintain full global tax compliance.