Introduction

Withholding Tax (WHT) is one of the most common taxes applied in Egypt on payments made to foreign entities for services, royalties, interest, and other cross-border transactions. Many multinationals end up overpaying WHT due to incorrect rates, missing treaty benefits, or misclassification of services and the only way to correct this is by filing a WHT refund request.

However, the WHT refund process in Egypt is highly documentation-driven, time-sensitive, and requires precise alignment with Double Tax Treaties (DTTs), Beneficial Ownership rules, and the Egyptian Tax Authority (ETA) requirements.

This guide outlines each step clearly, helping multinationals navigate the refund process smoothly and avoid delays or rejections.

1. When Are WHT Refunds Applicable in Egypt?

You may qualify for a withholding tax refund if:

✔ A tax treaty applies and offers a reduced rate lower than what was deducted

✔ WHT was deducted on non-taxable services

✔ WHT was applied incorrectly (e.g., service performed outside Egypt)

✔ The foreign entity qualifies as a Beneficial Owner under the treaty

✔ Duplicate deductions or miscalculations occurred

✔ WHT was erroneously withheld due to missing documentation during payment

WHT refunds primarily benefit:

-

Foreign service providers

-

Multinationals with Egyptian subsidiaries

-

Technology and consulting companies

-

Royalty/IP licensors

-

Loan interest recipients

-

Companies with cross-border intra-group charges

2. Understanding the Legal Framework

WHT refunds in Egypt are governed by:

✔ Income Tax Law No. 91 of 2005

✔ Executive Regulations (latest amendments)

✔ Double Tax Treaties signed by Egypt (over 60 treaties)

✔ ETA Beneficial Ownership and treaty-benefit rules

The ETA requires consistency between:

-

Contracts

-

Invoices

-

Payment flows

-

Nature of service

-

Treaty articles

-

Actual performance

Any inconsistency can lead to rejection.

3. Required Documentation for a WHT Refund in Egypt

This is the most important part of the process.

Mandatory Documents

✔ Official WHT certificates (Form 41)

✔ Proof of tax deduction and payment

✔ Original invoices issued by the foreign entity

✔ Contract or service agreement

✔ Bank SWIFT/transfer confirmations

✔ Passporting of payments to the foreign entity

✔ Tax Residency Certificate (TRC) from home country

✔ Beneficial Ownership declaration

✔ Explanation letter summarizing the refund request

✔ Power of attorney (if a local advisor submits the file)

Strong supporting documents

-

Evidence showing where services were performed

-

Timesheets or deliverables

-

Email correspondence

-

Any document proving business purpose

The stronger the documentation, the faster the refund.

4. Step-by-Step Refund Process

Below is the simplified, practical roadmap:

Step 1 Collect All Required Documents

Start by gathering:

-

Form 41

-

Invoices

-

Contract

-

TRC

-

Beneficial ownership certificate

-

Payment evidence

Missing documents are the #1 reason for delays.

Step 2 Perform a Treaty Analysis

Identify:

-

The applicable treaty

-

Relevant articles (Services, Royalties, Interest, etc.)

-

The correct WHT rate

-

Whether a Permanent Establishment (PE) exists in Egypt

-

Whether the foreign provider qualifies as Beneficial Owner

If the foreign entity fails the BO test → refund will not be accepted.

Step 3 Prepare the Refund File

This file must include:

✔ A cover letter summarizing the case

✔ A treaty analysis referencing treaty articles

✔ A calculation of the refund amount

✔ Full documentation package

✔ Explanation of the nature of the service

✔ Proof that the service was performed outside Egypt (if applicable)

Step 4 Submit the Refund File to the ETA

Submission is made to:

The Competent Egyptian Tax Office (based on payer’s location)

The ETA will:

-

Review documents

-

Request clarifications

-

Ask for additional support

-

Compare payments with Form 41 data

Step 5 Respond to ETA Queries

Expect follow-up questions from the ETA, such as:

-

Where was the service performed?

-

Does the provider have PE in Egypt?

-

Why was this WHT rate applied?

-

Is the foreign entity the actual Beneficial Owner?

-

Provide proof of payment to the foreign provider

Timely and well-supported responses increase approval chances.

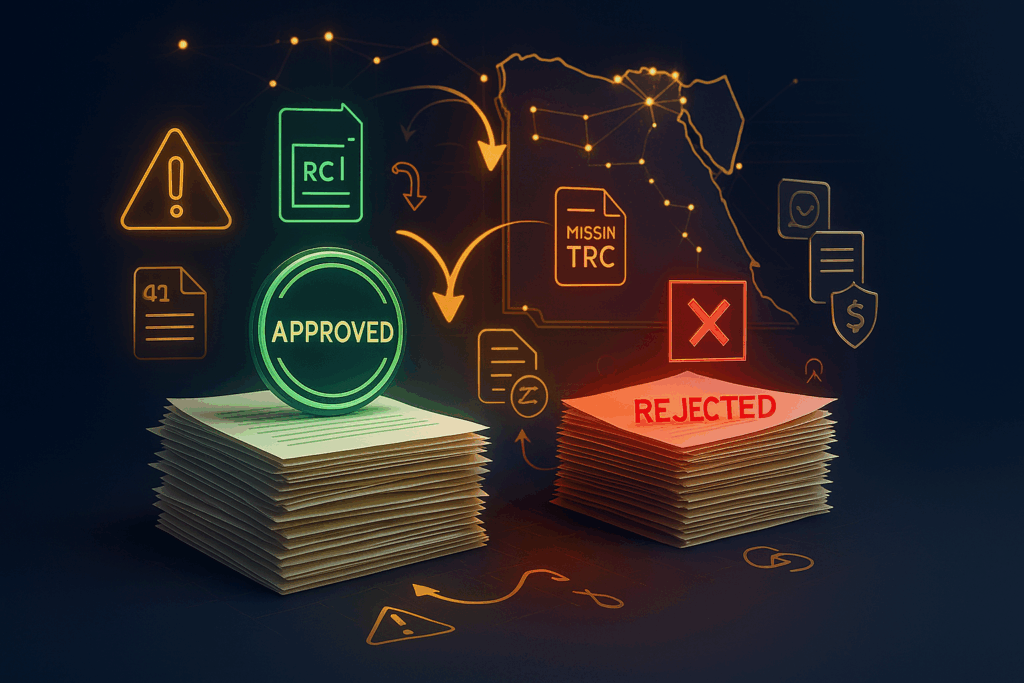

Step 6 ETA Issues Acceptance or Rejection

If accepted:

-

Refund is approved

-

Amount can be offset or refunded depending on case

If rejected:

-

You may file an appeal

-

Or escalate through dispute-resolution channels

5. Common Reasons for WHT Refund Rejections in Egypt

❌ Missing or expired TRC

❌ Failure to prove Beneficial Ownership

❌ Lack of evidence on where the service was performed

❌ Inconsistent invoices and contracts

❌ No proof of actual payment

❌ Treaty incorrectly applied

❌ Foreign entity has PE in Egypt

These must be avoided by preparing a proper audit-proof file.

6. Best Practices for Multinationals

✔ Apply for TRC early each year

✔ Ensure contracts reflect the actual service

✔ Maintain Form 41 and WHT certificates properly

✔ Document the business purpose of cross-border services

✔ Keep a centralized compliance folder

✔ Conduct a pre-submission technical review

✔ Respond to ETA queries with complete evidence

Conclusion

Applying for a withholding tax refund in Egypt requires strong documentation, accurate treaty analysis, and careful alignment with Egyptian tax rules. While the process is detailed and sometimes lengthy, companies that prepare a complete file and clearly demonstrate entitlement to treaty benefits have a high chance of success.

With proper guidance and proactive planning, Egyptian and foreign multinationals can recover overpaid WHT and maintain full compliance with ETA requirements.